[SMM Hot Topic] Intensified Overseas Trade Frictions—Is China’s Steel Export Volume Starting to Pull Back?

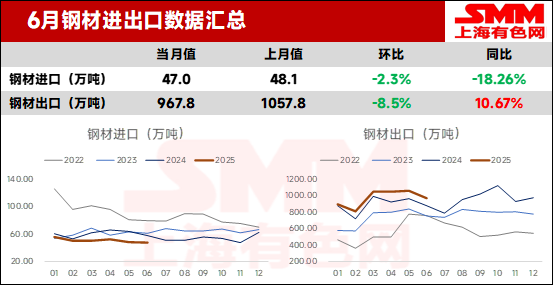

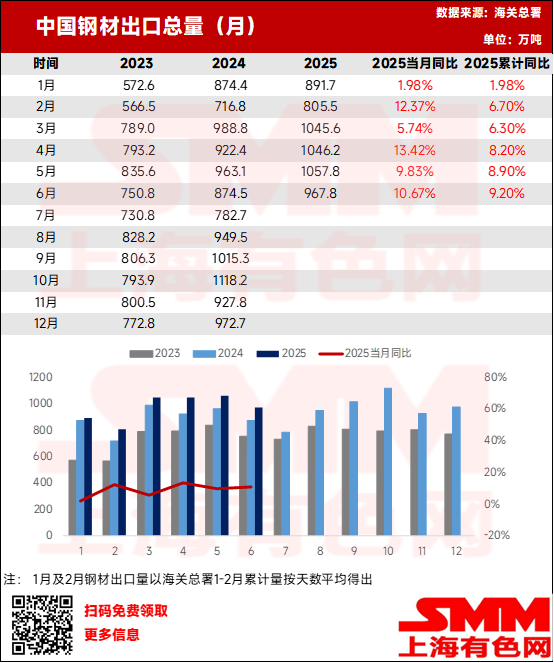

On July 14, customs data showed China exported 9.678 million mt of steel in June 2025, down 900,000 mt or 8.5% MoM; cumulative exports from January-June reached 58.147 million mt, up 9.2% YoY.

China imported 470,000 mt of steel in June, down 11,000 mt or 2.3% MoM; cumulative imports from January-June totaled 3.023 million mt, down 16.4% YoY.

June 2025 Steel Trade Data Overview

- China’s Steel Exports Fall Below 10 Million mt Threshold

China’s steel exports drop 8.5% MoM in June! On June 3, Brazil initiated anti-dumping investigations against HRC imports from China. Meanwhile, US President Trump announced a tariff hike on steel/aluminum and derivative products from 25% to 50%, effective June 4. Escalating global trade frictions persist, though domestic traders continue volume discount strategies to secure deals. However, overall order intake has pulled back amid weakening seasonal demand worldwide.

- China’s Steel Imports Show Modest MoM Decline in June

China imported 470,000 mt of steel in June, down 11,000 mt or 2.3% MoM; cumulative imports from January-June reached 3.023 million mt, down 16.4% YoY. Net steel exports stood at 45.916 million mt.

- Short-Term Steel Export Outlook

Global manufacturing PMI reached 49.5% in June 2025, up 0.3 percentage points MoM with two consecutive monthly increases, though remaining below 50%, per China Federation of Logistics & Purchasing. While global manufacturing stays in contraction territory, the marginal uptick signals improving recovery momentum. During the tariff hike suspension period, countries worldwide accelerated economic recovery efforts. China’s manufacturing PMI new export orders index stood at 47.7% in June, up 0.2 percentage points MoM with two consecutive increases.

World Steel Association monitoring shows global crude steel production (70 countries) reached 158.8 million mt in May 2025, down 3.8% YoY. China produced 86.55 million mt (-6.9% YoY), while production outside China reached 69.7 million mt (+0.37% YoY).

As of July 14, 2025, FOB export offers for HRC stood at $550/mt (India), $535/mt (Turkey), and $455/mt (CIS). China’s HRC export offer was $464/mt, creating price differentials of $86/mt, $71/mt, and -$9/mt against these countries respectively. After recent domestic favorable news drove up prices through speculation, both domestic and foreign trade prices surged significantly. However, as the off-season gradually deepened overseas, downstream consumption weakened, and some traders reported difficulties in moving goods at higher prices. As a result, prices fluctuated rangebound, and the price spread between China's and other countries' HRC export offers narrowed accordingly.

According to the latest SMM survey on steel mills' export order scheduling, under the export task of maintaining volume, the planned HRC export volume for July increased slightly MoM compared to the actual export volume in June. However, with the contraction of the price spread between domestic and overseas markets, the price advantage of China's steel exports weakened somewhat. Coupled with the weakening global demand, domestic order-taking pressure increased. Therefore, SMM expects that the total steel exports in July will continue to decline compared to June but will remain at a relatively high YoY level.

As July began, with the continuous deepening of global trade frictions, the risks faced by China's steel exports continued to increase. On July 4, 2025, Vietnam's anti-dumping investigation on HRC imports from China moved from preliminary to final ruling. Meanwhile, the Malaysian government preliminarily ruled to impose temporary anti-dumping duties on galvanized steel coils/sheets originating or exported from China, South Korea, and Vietnam, with tariff rates ranging from 3.86% to 57.90%. Additionally, considering the escalation of the US's imposition of reciprocal tariffs globally, this will continue to exacerbate the crisis in domestic steel re-export trade.

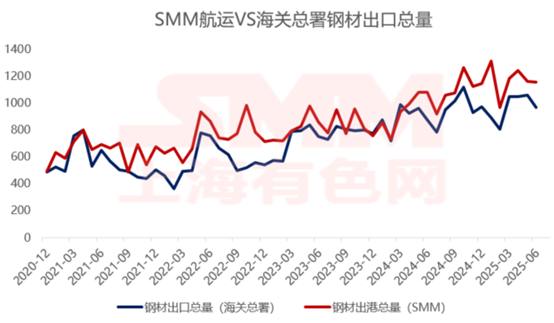

According to SMM shipping data, as of June 31, the total port departures from Chinese ports in June were 11.5429 million mt, down 0.55% MoM from May, with a smaller decline compared to customs data, possibly due to the still high volume of steel billet exports in June. Meanwhile, according to the SMM survey, recent export order-taking for HRC, steel billets, and other products has pulled back. Although domestic prices have surged with the futures market, it is not easy to secure orders at higher export prices. The situation of export MD (missing delivery) remains rampant. Under the influence of malicious competition, it is difficult for traders to close deals. In summary, SMM expects that steel exports in July will still maintain a relatively high YoY growth level but will continue to decline compared to the total export volume in June. On the basis of maintaining export volume, the decline should not be overly pessimistic for the time being.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)